UK Investment Trust vs ETF vs Stocks

I've written a couple of posts about spread betting as my preferred method of investing in the stock market due to its tax benefits. Most people will overlook it though as it's got betting in its name. Maybe if they rebranded it to spread investing, then more people would open accounts and avail the benefits of tax-free investing (gambling).

The stock market is a great place to invest money for the long term or gamble in the short term. There isn't really much of a distinction, I am sure it's just the expected return and variance that differentiates the two. So day trading is gambling as the returns are unknown on the day and the variance is high. For long term investments, you can forecast the stock market will grow say, 5% a year, so long term your expected return is positive and if you track an index, the variance going to be small.

The main ways to invest in the stock market are buying shares directly, active funds or passive funds. Shares, you just pick what you think will provide a good return in terms of capital growth and dividends. Active funds, someone takes your money and invests for you but take a fee, an investment trust can be considered an active fund. Passive funds, just track an index or several indices. These will charge lower fees, so have become very popular over the last few years.

Inside or Outside a tax wrapper

If you investing in a pension, the returns are tax-free until you withdraw so you don't need to worry about the tax treatment. In the UK they have ISAs where the returns are tax-free too. If you are in Ireland and have not maxed out your pension contributions, I would recommend getting a non-standard PRSA, which is like a SIPP (Self invested personal pension) in the UK. You can invest in individual stocks and funds via the pension and avail yourself the tax benefits. Inside a tax wrapper, there isn't much between the options, Investment trust vs ETF vs Shares. Its a matter of personal preference and people have a mixture of all 3. In my UK SIPP, I have some investment trusts and shares and all returns are tax-free until I want to withdraw.

Outside a tax wrapper, the case for an ETF is very weak to the point where they are not worth buying. More later.

Expect return and variance

The stock market over the long term is expected to generate a positive return. It is important to talk about specific stock markets though. The UK FTSE 100 has only kept up with inflation for the last 20 years whereas the USA stock market has grown well above inflation. Some people talk about the stock market as one monolithic beast when it's not. It's just easier to talk about general returns, just be aware if you choose the wrong indices, you might not make anything, even over a decade or two.

So stocks in the long term generate a positive return, you just don't know which ones in advance. There are things called indices that track a basket of shares on a stock market, for example, the FTSE 100 tracks the 100 biggest companies on the London stock exchange. Or the S&P 500 which consists of 500 companies in the USA. These appear as a weighted index and you can track the overall performance of the stock market using one of these. Some stocks will do better, some worse but overall performance is reflected in the index.

You can choose stocks if you wish but the general consensus is that the market is very efficient and beating the index is very hard to do over the long term. Your return might higher and higher variance if you buy individual stocks. Most people prefer a steady return with lower variance even if its lower than if you were stock picking.

Why ETfs?

ETFs are low-cost ways to track an index. There are other types of ETFs that are actively managed or concentrate on a sector but usually, people mean low-cost index trackers and so I will use it to mean that too. Nothing really wrong with this approach. You could argue there is a bubble in passive investing as you are buying things because they are in an index rather than they are any good. Thats open to debate though.

The main problem with ETFs is the tax treatment. At 41% the tax is high, and every 8 years you got to pay tax as if you had sold. This kills the ability to compound. Outside a pension, investment trusts are so much better.

Why Investment Trusts?

Investment trusts are companies that buy shares in other companies and trade themselves on the London Stock market. The most famous one is Scottish Mortgage Trust which has nothing to do with Scottish Mortgages nowadays. They invest in a wide range of companies on your behalf and charge you a fee for it. These have outperformed their benchmarks for years. You can find out more here on the AIC website.

Basically, you get the diversity of an index without the high taxes. The downside is that fees are higher as you have someone actively managing your investment. Fees can eat into any investment return but some of these trusts have outperformed indices for decades net of fees.

Why Stocks?

Picking stocks is somewhat risker than buying an ETF or Investment Trust. You can make more money if you are right though. Its pretty obvious to me tech and property are going to be big winners over the next decade, so I have biased my portfolio to these sectors. Can you really imagine a world where Amazon and Google don't outperform the average company?

I might be wrong on this but I am willing to take a chance. In life, we are generally encouraged to have an opinion and act upon it. With investing though, the consensus is that you will fail and so take the average.

Conclusion

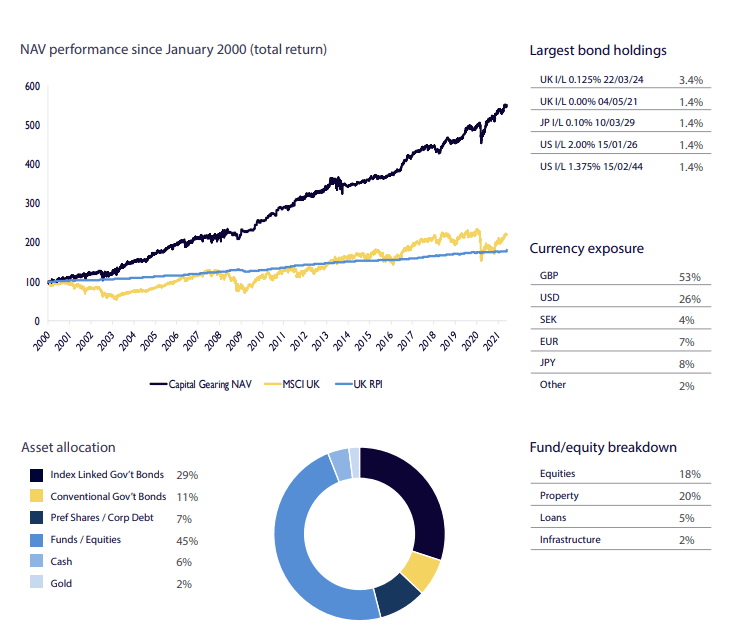

If you want a diversified portfolio with low variance investment trusts outside a pension are better than ETFs due to their tax treatment. Even after fees, some investment trusts have outperformed their benchmarks for decades. One to get your started is Capital Gearing To preserve the real wealth of shareholders and to achieve absolute total return over the medium to longer term through investment in quoted closed-ended funds and other collective investment vehicles, bonds, commodities and cash.

Totally trounce the performance of the MSCI UK benchmark. UK equities have been awful for the last 20 years.

If you have a higher risk tolerance and time to research, individual shares may be better for you. I can't imagine anyone losing out long term buying Google stock.

Ben Luong is a technical marketing consultant who operates where AI falls short. In a world flooded with cheap, mediocre code and automated strategies, he provides the expert integration, verification, and strategic accountability required to make modern marketing stacks profitable. He specialises in architecting Google Ads, SEO, and GA4 into a single, high-performance system that is accountable to the bottom line.